The tax advantages of Malta holding companies

03 October 2018

Malta holding companies are an attractive option for international trading groups. Dixcart Management Malta explains.

The location of a holding company needs to be considered carefully in any international structure where one of the aims is to minimise tax on income flow. In this article, Henno Kotze explains what makes Malta an attractive option.

Advantageous characteristics for international holding company locations

Ideally the holding company should be resident in a jurisdiction which:

- Has a good double tax treaty network, thereby minimising withholding tax on dividends received

- Exempts dividend income from taxation

- Does not charge capital gains tax on the disposal of subsidiaries

- Does not impose withholding tax on distributions from the holding company to its parent or shareholders

- Does not impose capital gains tax on profits arising from the sale of shares in the holding company by non-resident shareholders

- Does not impose capital duty on the transfer of shares

- Has certainty of tax treatment

Malta holding companies can benefit from all of the above.

Malta holding companies - the advantages

Malta has a network of over 70 double tax treaties.

In most situations where a Malta company owns more than 10% of the issued share capital of an overseas subsidiary, the rate of withholding tax on dividends received by a Malta company from a treaty partner is reduced to 5%.

As Malta is part of the EU, it also benefits from the EU Parent/Subsidiary Directive, thereby reducing withholding tax to zero on dividends from many EU countries.

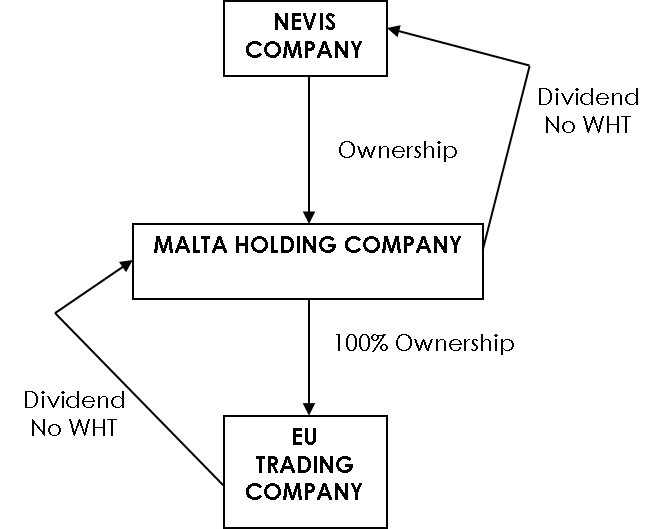

In the example on the left, where the trading company is situated in the EU, the Malta company would benefit from the EU Parent/Subsidiary Directive, resulting in no withholding tax on the payment of dividends to the Malta company.

Where the holding is a “participating holding” there will be no taxation on dividends and capital gains at the Malta holding company level.

Dividends can therefore be paid to the Nevis company without any deduction of tax.

Malta holding companies: available tax efficiencies

Participation exemption and capital gains tax exemption

Qualifying dividends and capital gains derived from a “participating holding” are (at the option of the taxpayer) exempt from Malta tax.

The Budget Implementation Act (2018) introduced changes to the treatment of shareholding participations, reducing the applicable tax rate from 10% to 5%.

In order for a holding to be classified as a ‘participating holding’, one of the following conditions must be satisfied:

- the company holds directly at least 5% of the equity shares of a company not resident in Malta, OR

- the company is an equity shareholder in a company not resident in Malta and has the option to acquire all of the equity shares, OR

- the company is an equity shareholder in a company not resident in Malta and is entitled to first refusal on any proposed disposal, redemption or cancellation of the equity shares of that company, OR

- the company is an equity shareholder in a company not resident in Malta and is entitled to either sit on the Board or appoint a person to sit on the Board of that company as a director, OR

- the company is an equity shareholder and invests a minimum €1,164,000 in a company not resident in Malta. This investment must be held for an uninterrupted minimum period of 183 days, OR

- the company is an equity shareholder in a company not resident in Malta and the holding of shares is to further develop business for that company, not as trading stock.

Additional anti-abuse provisions are applicable.

Please speak to our Dixcart office in Malta: advice.malta@dixcart.com for a definition as to what constitutes a participating holding.

Sale of shares in the holding company

Malta does not charge capital gains tax on the sale of shares in Malta companies.

No withholding tax

Malta does not impose withholding tax on the distribution of dividends to shareholders or parent companies.

Zero withholding tax is applicable, regardless of where in the world the shareholder is resident.

No capital duty

In Malta there is no capital duty on the issue of share capital and there is no stamp duty payable on subsequent transfers.

Other income

Income other than dividends and capital gains is subject to tax at Malta’s normal rate of 35%. However, on payment of a dividend from this “other income”, a tax refund of between 6/7ths and 5/7ths of the tax paid by the Malta company is payable to the shareholder. This results in a net Malta tax rate of between 5% and 10%.

Where such income has benefited from double tax relief or the Malta flat rate tax credit, a 2/3rds refund applies.

READ...

Certainty of tax treatment

It is possible to obtain formal tax rulings in Malta. Rulings provide certainty on a specific transaction and the application of the law, and are binding on the Malta Revenue for five years.

There is also a system of informal Revenue guidance. This takes the form of a letter of guidance from the Revenue. Such letters are not expressly regulated by law, but create a legitimate expectation on which a taxpayer can rely. The Malta Revenue Authorities consider such letters as binding.

Conclusion

A Malta holding company is an attractive option for international trading groups.

The potential advantages include:

- The benefits available through Malta’s extensive double tax treaty network

- Exemption of dividends from taxation in Malta.

- Exemption from capital gains tax on the disposal of participating holdings.

- The absence of capital gains tax on the sale of shares in a holding company by foreign shareholders.

- The absence of withholding tax.

Contact

If you would like further information on this subject, please contact the Dixcart office in Malta or your usual Dixcart contact.